What are the main mortgage rules in Canada? Our guide to what you should know before you get your next home.

Wed Aug 09 2023 18:55:00 GMT+0000If you're a new homebuyer seeking a mortgage, or an existing homeowner looking to switch or refinance, it's important that you're up to date on the mortgage rules in Canada. These include the Canadian Mortgage Stress Test changes made in 2021 and the Prohibition on the Purchase of Residential Property by Non-Canadians Act, nicknamed the Foreign Buyers Ban, passed in 2022 and recently amended in March 2023. Here are some of the top things you should keep in mind about mortgage rules in Canada if you're looking for a new home.

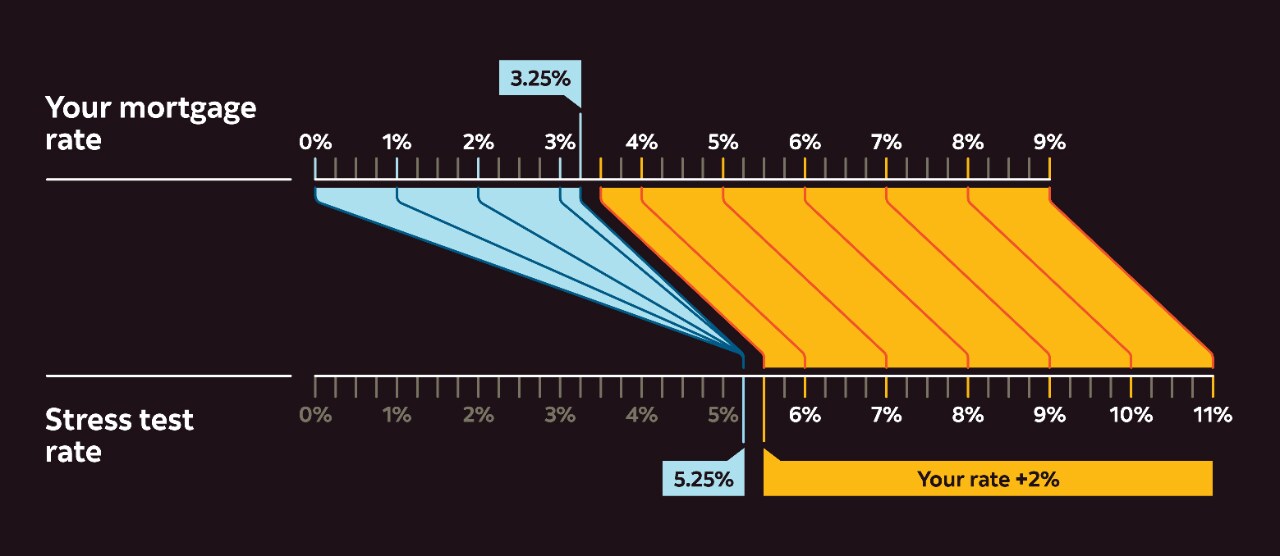

The mortgage stress test was introduced on January 1, 2018, as a way to protect Canadian homeowners. It requires banks to check that a borrower can still make their payments at an interest rate that's higher than they will actually initially get. The purpose of the stress test is to evaluate if a borrower (a.k.a. the potential homeowner) can handle a possible increase in their mortgage interest rate. For Canadians to qualify for a federally regulated bank loan, they need to pass the mortgage stress test. To do this, homebuyers need to prove that they can afford a mortgage at a qualifying rate that’s higher than the rate they are approved for by their lender. The stress test was revised in June 2021. As of June 2021, that rate has been either the interest rate they were approved for by their lender plus 2%, or 5.25%, whichever is higher.

For example, if your mortgage rate is 2%, then the stress test would require that you be able to afford the mortgage at a rate of 5.25%, since that's higher than 4 % (the approved rate plus 2%). If the rate approved by their lender is 5%, however, the mortgage stress test would require that the buyer be able to qualify for the home at a rate of 7% (ex. the approved rate of 5% plus 2%).

This stress test is also performed with homeowners looking to refinance, take out a home equity line of credit or change mortgage lenders. Those who renew with the same lender don't have to undergo the stress test again. This change in mortgage approvals has meant that borrowers may end up only qualifying for lower mortgage amounts. This is because of the higher qualifying rates as a result of the stress test. Learn more about the stress test here.

In June 2022, Canada introduced regulations that would ban non-Canadians from directly or indirectly purchasing residential property in Canada for a period of two years (this ban started on January 1, 2023). The legislation, called the Prohibition on the Purchase of Residential Property by Non-Canadians Act, is meant to cool housing prices for the benefit of Canadians. For that reason, foreign buyers will not be able to qualify for a mortgage in Canada during this two-year period. It's also expected that the government may implement additional regulations on foreign ownership after the two-year period expires. The regulations went into effect in January 2023 and require those violating it to pay a fine of $10,000. The government could also order the sale of the property. However, in March 2023, the government amended the legislation to make it easier for newcomers to Canada on work permits to purchase property. Work permit holders are eligible to buy a home if they have at least 183 days left on their work permit, and they have not purchased more than one residential property. The regulations also no longer apply to vacant land or property purchased for development purposes. If you are concerned about how this legislation might affect you, reach out to your legal advisor.

Homebuyers with a down payment of less than 20% of the purchase price are required to purchase mortgage default insurance. This means you could get mortgage default insurance from either Canada Mortgage and Housing Corporation (CMHC), Sagen or Canada Guaranty. However, all three providers have declared that properties costing $1 million or more aren't eligible for mortgage default insurance. All three mortgage default insurance providers also offer limits on the types of properties you can purchase with their insurance. For example, options like short-terms rentals, units used for a hotel or mixed-use properties are ineligible. Learn more about how mortgage default insurance works here

The 2021 CMHC rules affect the amount of debt that borrowers with a default insured mortgage can carry. Mortgage applicants will be limited to spending a maximum of 39% of their gross income on housing and can only borrow up to 44% of their gross income once other loans payments are included. This is up from the previous 35% and 42% set in 2020. These amounts can change frequently so be sure to double check what they currently are on the CMHC website.

Are you looking into which mortgage is right now you? A mortgage calculator can help give you an idea of how much you can qualify to borrow towards a mortgage. However, mortgage calculators can't tell you how much you could actually borrow, because you don't know what mortgage interest rate you're likely to qualify for. To fully understand your home buying budget, you'll need to apply to be pre-approved for a mortgage. A Scotiabank Home Financing Advisor can help you apply for a pre-approval. They can also advise on strategies for things like saving for a larger down payment or how to use your existing funds more effectively – for example, taking advantage of options like your RRSP's Home Buyer's Plan or the Tax-Free First Home Savings Account.